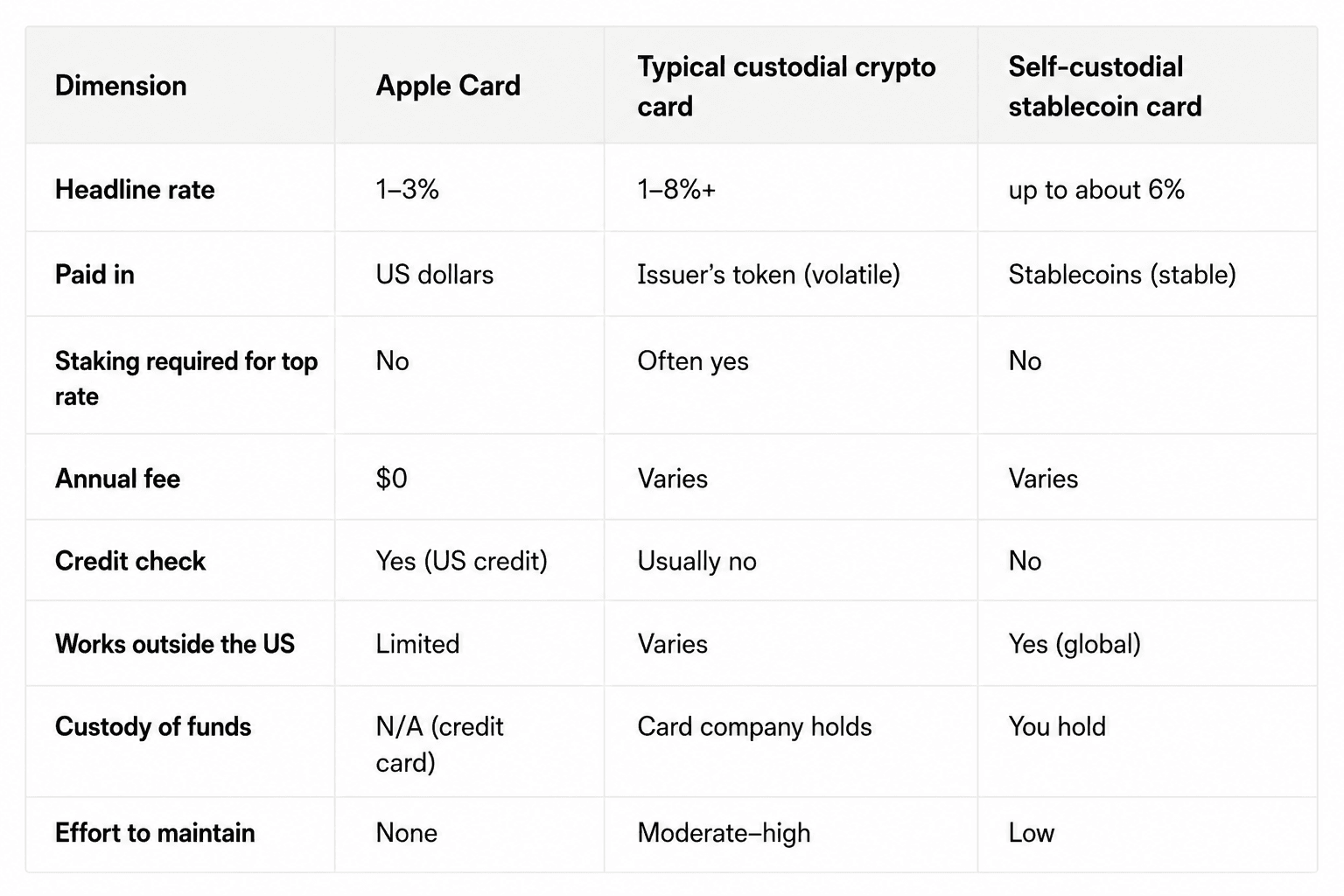

Short answer: Apple Card gives consistent, uncapped rewards - 3% on Apple and select partners, 2% on Apple Pay, 1% on the physical card - paid in dollars, with no fees and no conditions. Crypto cashback cards advertise much higher rates (up to 8% on some, 20% on a few), but the realized rate for most users lands around 1-2.5% once you account for caps, staking requirements, and token volatility. The exception is a self-custodial card that pays cashback in stablecoins with no staking lock-up - that's the one category that genuinely beats Apple Card on rewards while staying predictable. Which one wins depends entirely on who you are.

This post does the honest math. Not headline rates - what you'd actually keep after 12 months of real spending.

How Apple Card rewards actually work

Apple Card is the benchmark most people compare against, so it's worth being precise about what it actually pays.

The 3% / 2% / 1% tier structure

Apple Card Daily Cash works in three tiers as of 2026:

- 3% on purchases from Apple (App Store, Apple Music, Apple TV, hardware) and from a rotating list of select partners when you use Apple Pay - currently including Uber, Uber Eats, Nike, Walgreens, Booking.com, Exxon, Mobil, Hertz, and Ace.

- 2% on anything else when you pay with Apple Card through Apple Pay.

- 1% when you use the physical titanium card or the virtual card number anywhere Mastercard is accepted but not through Apple Pay.

There's a $0 annual fee, no foreign transaction fee in most cases, and the cash is uncapped - there's no monthly limit on how much you can earn.

What Apple Card gets right

The reason Apple Card is the card to beat: the rate you see is the rate you get, every time, with zero effort. No staking. No tokens to hold. No tiers to unlock. The Daily Cash is paid in US dollars, so a 2% reward is worth exactly 2% - it doesn't move with a token price. For a US user who lives inside Apple Pay and has good credit, that consistency is genuinely hard to beat.

The honest limitation: most everyday spend earns 1–2%, not 3%. The 3% is concentrated on Apple's own products and a partner list. Realistic blended cashback for a typical spender sits around 1.5–2%.

How crypto cashback cards actually work

Crypto cashback cards are where the headline numbers get loud - and where the gap between advertised and realized rewards gets widest.

Headline rates vs realized rates

The advertised rates look spectacular next to Apple Card's 1–3%. Different cards in 2026 advertise anywhere from 2% up to 20%. But across the category, effective after-fee rewards for typical everyday spend cluster around 0.8%–2.5% unless you commit to staking or hit a high annual spend threshold. The headline is almost always the top-tier rate available to a small fraction of users.

The hidden conditions

Three things sit between the headline rate and what you keep:

- Staking and tier-locking. The highest crypto card rates usually require holding or staking thousands of dollars in the issuer's native token. That capital has its own price risk, separate from the cashback.

- Monthly caps. Many crypto cards cap rewards per month at each tier. A "10% cashback" card capped at $50/month is effectively a much lower rate for anyone with real spend.

- Token volatility. Cards that pay cashback in a native token expose you to that token's price. A 5% reward paid in a token that drops 40% before you sell is, in practice, a 3% reward.

This is the core insight most comparisons miss: a crypto card's advertised rate tells you almost nothing about what you'll keep. You have to look at the payout currency, the cap, and the unlock conditions.

The honest math: what would you actually earn?

Take a user spending $2,000/month - $24,000 over 12 months - and run the realistic numbers.

Apple Card realistic 12-month payout

Most of that $24,000 earns 1–2% (2% via Apple Pay, 1% on the physical card, 3% only on Apple and partners). A realistic blended rate is roughly 1.75%. That's about $420/year, paid in US dollars, uncapped, at full value, with zero effort.

Custodial crypto card (no-staking tier) realistic payout

A typical custodial crypto card at its no-staking tier pays about 1% in the issuer's token. $24,000 × 1% = $240/year in a volatile token. Apply a conservative 20% volatility discount and you realistically keep around $190/year - less than Apple Card, with more effort.

Self-custodial stablecoin card realistic payout

A self-custodial card that pays cashback in stablecoins at roughly a 5% blended rate, with no staking requirement, returns $24,000 × 5% = about $1,200/year, retained at full value because stablecoins don't move. There's no token to hold and no lock-up. On cards where the underlying balance also earns yield while it waits to be used, the effective return is higher still.

What it looks like at higher spend

The gap widens as spend goes up, because Apple Card's blended rate stays flat while a stablecoin card's advantage compounds. Take a heavier spender at $5,000/month - $60,000/year:

- Apple Card at roughly 1.75% blended = about $1,050/year, in dollars, uncapped.

- Custodial crypto card at roughly 1% after volatility = about $480/year.

- Self-custodial stablecoin card at roughly 5% = about $3,000/year, plus any yield earned on the balance while it waits to be used.

At $5,000/month the difference between the best and worst option is roughly $2,500/year. For a high-spend user - a digital nomad, a freelancer running expenses through one card - the choice of card stops being a rounding error and starts being real money.

The pattern is clear. Apple Card comfortably beats a bad crypto card. A good self-custodial stablecoin card comfortably beats Apple Card on raw rewards. The headline rate was never the thing that mattered - the payout currency and the conditions were.

Apple Card vs crypto cashback card: side-by-side

Who Apple Card is best for

Apple Card is the right call if you:

- Are in the US with good credit.

- Do most of your spending through Apple Pay.

- Want zero maintenance - no tokens, no staking, no tiers.

- Value a reward that's paid in dollars and never moves.

- Spend meaningfully at Apple or its 3% partners.

For that profile, Apple Card's consistency is genuinely excellent and most crypto cards are not worth the added complexity.

Who a crypto cashback card is best for

A crypto cashback card is the better choice if you:

- Want a meaningfully higher realized rate, not just a higher headline.

- Spend internationally or outside the US, where Apple Card coverage thins out.

- Don't have or don't want to use US credit.

- Already hold crypto and want the card to draw from a balance you control.

- Prefer cashback in stablecoins (predictable) over a volatile token.

The critical caveat: this only holds for the right crypto card. A custodial, token-cashback, staking-gated card is usually worse than Apple Card. A self-custodial, stablecoin-cashback, no-staking card is the one that wins.

Where Tria fits

Tria is one example of the self-custodial stablecoin-cashback category - the one that closes the gap with Apple Card and then moves past it on raw rewards. The Tria Card pays up to 6% cashback in stablecoins, with no token to stake and no lock-up window, so the rate you see is the rate you keep. It's a self-custodial Visa card usable in 150+ countries, and the balance behind it can earn yield through Tria's Earn product up to the moment you use the card - so the funds do two jobs at once.

To be fair about it: Tria won't replace Apple Card for a US user who lives in Apple Pay and wants zero maintenance. It's built for the user the second profile above describes - global, crypto-native, self-custody-minded. If that's you, the realized-rewards math favors a card like Tria by a wide margin.

Download Tria to set up a card-ready balance.

Frequently asked questions

Is Apple Card or a crypto card better for cashback?

It depends on the user and the specific crypto card. Apple Card pays a consistent blended rate of around 1.75% in dollars with zero effort - hard to beat for a US Apple Pay user. A self-custodial crypto card paying roughly 5% in stablecoins with no staking beats Apple Card on raw realized rewards. A custodial crypto card at a no-staking tier paying in a volatile token is usually worse than Apple Card. The payout currency and conditions matter more than the headline rate.

Why is a crypto card's realized cashback lower than its advertised rate?

Three reasons: the headline is usually the top-tier rate that requires staking thousands in the issuer's token; many cards cap monthly rewards at each tier; and cards that pay in a native token expose you to that token's price, so a drop between earning and selling cuts the effective rate. Cards that pay in stablecoins with no staking avoid all three.

Does Apple Card work outside the United States?

Apple Card is a US product. It can be used internationally where Mastercard is accepted, but it's designed around the US market, US credit, and US Apple Pay partners. For users who spend primarily outside the US, a globally usable crypto card often delivers better real-world value.

Do crypto cards require a credit check like Apple Card?

Generally no. Apple Card is a credit card and requires a US credit check. Most crypto cards are debit-style - funded by your own balance - so they don't require a credit check or credit history, which makes them accessible to users Apple Card can't serve.

Which card is safer for my money?

Apple Card is a credit card, so the "money" question is about credit terms, not custody. Between crypto cards: a custodial card holds your funds, exposing you to the company's solvency; a self-custodial card keeps the funds in a wallet you control until each charge clears. For users who care about custody, the self-custodial model removes the counterparty risk a custodial card carries.